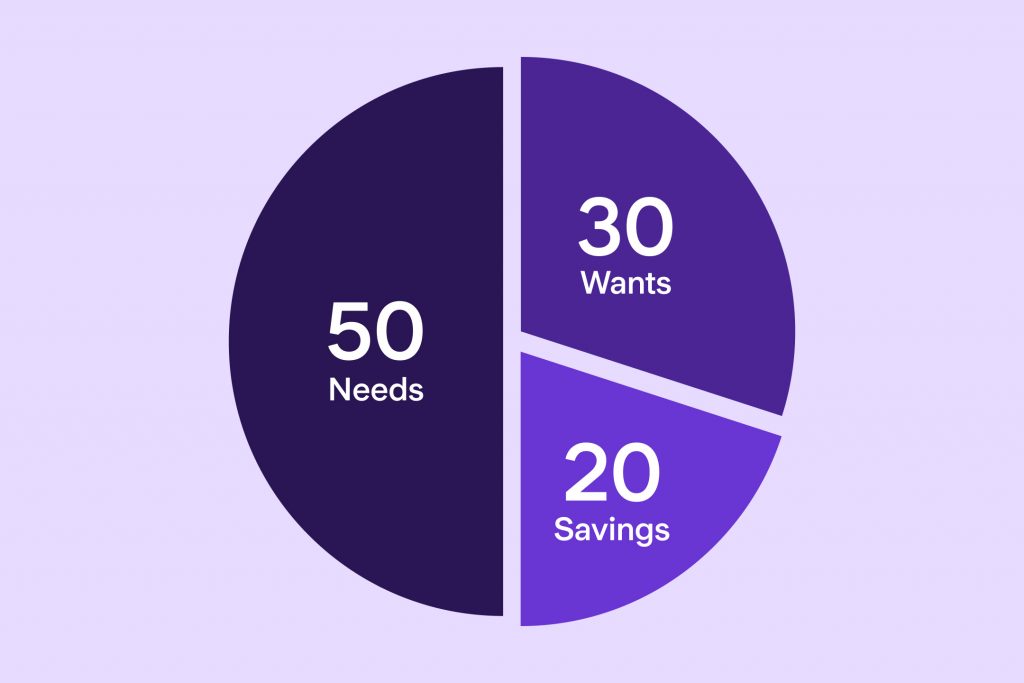

The 50 / 30 / 20 rule is a relatively simple budget method that allows an individual to allocate net income into 3 respective categories.

These being 50% for needs (so call essential living costs), 30% for wants (discretionary or leisure spending) and 20% for savings / debt.

This simple formula or framework, allows somebody to attain some financial balance or guidelines into how they should manage or locate their salary or income. With the aim to prioritise your essential needs first, whilst covering the desire to save funds or build wealth or assets for the medium or long term future.

So what are the key components:

- 50% – needs: essential and necessary living costs such as mortgage, rent, utilities (gas / elec / water), food, life and house insurance and transportation costs

- 30% – wants: non-essential spending so eating out, drinks and entertainment, leisure or sports, hobbies and subscriptions (netflix, spotify, broadband, gym membership etc)

- 20% – savings and debt: your financial goals, emergency fund, savings and investments, workplace or private pensions. With regard to debt it should at least exceed the minimum amount required by your lender.

So how can we calculate these amounts:

- Calculate your monthly net income or salary across all sources (i.e take home pay)

- Track your spending – log or record where your spending goes each month by creating a simple spreadsheet.

- then make adjustments accordingly, so your funds are going to the right categories.

If may appear daunting a first as you may never have tracked your spending in the past. Plus you will be surprised at your initial results and where your money is going.

But patterns will emerge and you can adjust and change your spending habits accordingly as you progress.

It may be that you find a lot of money going on socialising or entertainments, or on specific hobbies.

It may be you have a lot of credit debt or large car loan to cover.

Or it could be that you are living paycheck to paycheck and forever accessing an overdraft each month.

What are the common mistakes or pitfalls !

- high cost of living costs associated with mortgage or rent to cover where you live. Do you live in a city where costs are significantly higher. Do you live in a property that meets your needs, or it is too big for you.

- learn to get in the habit of savings – most people get the idea of savings wrong they save money after that had already enjoyed themselves. You should automate your savings and set up standing orders or direct debits each payday. I personally use the 1st of each month, but get into that habit of saving constantly on a regular basis.

- At first you should create an emergency fund of between 3 to 6 months expenditure to cover any undue costs or emergency repair within the household or against a car. I personally like to have at £ 1,000 set aside in simple easy access account available instantly. But my partner also has higher level of emergency money set aside.

- Try and reduce any outstanding debts – Are you paying high interest rates against credit cards, which may be in excess of 20%, whereby you are only making the minimum each month so that debt isn’t being reduced.

- There are so called good debts, such as mortgage or interest free loans (offered by shops / retailers etc) when normally making large or big ticket items so use them to your advantage. You should be aiming to clear any excessive debt repayments as your 1st priority.

- When that is done you can the allocate the money into your savings to make it work for you, not against you.

- finally, get involved in your finance and learn to improve your financial knowledge and awareness. To most people the idea of finance is confusing and complex but it shouldn’t have to be that way, but it’s not taught in schools or the workplace.

A simple example:

If £2,000 comes into your account each month, this means £1,000 would go towards your

‘needs’ – rent, council tax, energy bill, food and transportation, or commuting to and from work. This would leave you with £600 to spend on what you want and £400 to pay down credit card

debt, or set aside for an emergency fund, in case something expensive breaks and you

urgently need to fix it.

You fun money could be for socialising, holidays, birthdays, entertainments etc.

Or you could use the 20% (£400) to invest elsewhere such as within a Cash ISA, stocks and shares ISA, premium bonds etc. To create wealth or financial nest egg in future. Or you may invest that money within a pension plan towards your retirement. You could even use those savings to overpay your mortgage and pay it off earlier than expected.

Imagine being mortgage free, which is most people’s biggest monthly expense item.

Making the most of your 20%

- savings – whereby you have stability over short and medium term goals with flexibility

- investments – creating assets that grow and produce wealth in future years

- pensions – building a pot of money to fund later years when not working.

- remember to put funds into tax free wrappers such as ISA / Stocks & shares ISA, SIPP (personal pension) so growth is tax-free away from the HMRC.

Ideally how much should I save !

The idea of saving 20% for most people is beyond reach or comprehension, especially now as we are living in a cost of living crisis and taxes forever seem to be increasing year on year.

It may be that you start of small and increase the % saved and you adapt to your new spending habits. Unfortunately in the UK we have a low savings rate compared to other countries, in a recent survey. The UK has an average saving rate of 4.7%.

So how to get started with budgeting !

Get a notebook or create a simple spreadsheet, highlighting all income received against items of expenditure. Then divide into respective 3 categories (needs / wants / savings). Remember to record all items against each sector, so food, transport, meals out, utilities and you will see a simple pattern emerge over say a 3 month period. You will be surprised at where your money is going or being wasted.

If you have a partner or are married, then track items for both parties. It may be that you become organised and financial savvy, but does your partner have the same ideas, traits etc. Do you both have the same goals or ambitions financially, are on you the same path or journey ?

You could use a simple calculator such as those on the free and impartial moneyhelper website being: https://www.moneyhelper.org.uk/en/savings/how-to-save

Although most banks or apps, are now introducing budget and savings tools to help you, so check with your current bank provider.

You could try something called Zero-based budgeting !

In that you allocate 100% of your income to various categories so that you have a balance of

zero at the end of each month, you’ll be doing what’s known as zero-based budgeting.

Whereby every pound that you have has a specific purpose and isn’t wasted.

Different methods work for all people, but try and find a simple solution to your specific needs. the hardest part for anyone is getting started and taking ownership of where your money goes.

And remember your goals, aims and financial objectives relate to you, and don’t compare yourself to work colleagues or friends. Avoid lifestyle creep and try not to keep up with the Joneses.

Some people may appear to be well off, by having expensive holidays or nice cars on their driveway, but they may be hiding behind a mountain of personal debt. They may have no savings or emergency fund in the background and could be living payday to payday. But they have created an illusion to others that they appear rich. They could be 1 step from financial ruin, if they lost a job or made redundant as simple example.

Remember: Hopefully you found this blog post useful and informative, and has given you some ideas towards improving your financial knowledge and well being.

Check out my other blogs posts on savings, pensions, investing and investment books that I recommend on https://moneyminted.co.uk. So you too can reach your financial goals and aims in future.

The world of personal finance and investing, is not a get rich quick scheme, but you can achieve your financial goals and dreams if you thing long term and invest within tax free wrappers.

Be the first to reply